With 20 years in the flooring industry in various roles in the U.S. and in Europe, China, Canada, and Brazil as CEO, Board Director, Interim CEO, and an advisor to boards and CEOs, I have experienced many market cycles. At the 2025 Tile Solutions Plus conference, I offered my perspective on the tile industry and my outlook for 2026.

There are many uncertainties, but there are reasons to believe the worst is coming to an end. The challenge is managing carefully through the uncertainty until demand recovers.

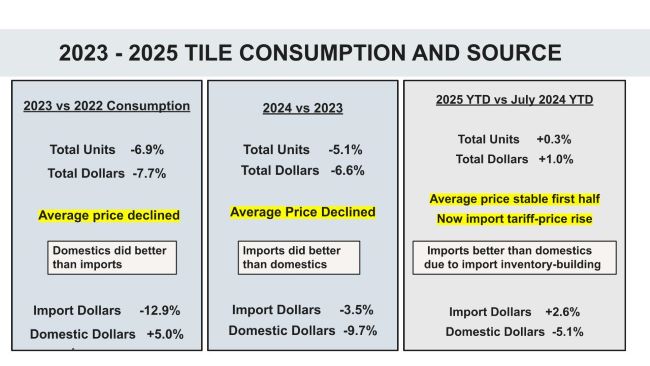

Three difficult years—though tile held up better than most

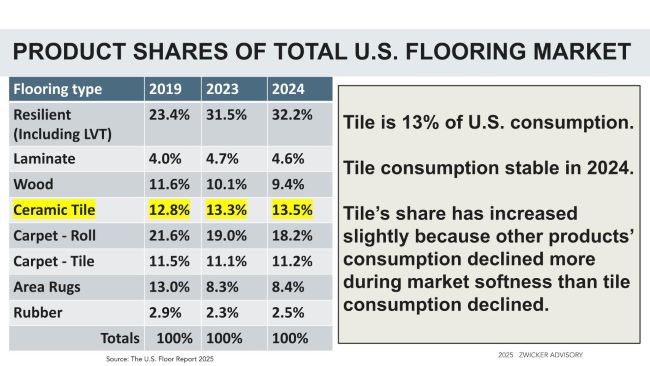

Despite optimistic predictions, demand never recovered in 2023, 2024, or 2025. While overall flooring sales in 2025 were down roughly 4%–5% year-to-date, tile demand stayed essentially flat. That is a relative victory. Tile’s share of the total U.S. flooring market is 13%, and in the past few years increased slightly as other product categories declined more sharply.

Looking ahead, tile demand in 2026 is likely to land somewhere between –3% and +3%—essentially a flattish year, with any upside or downside coming from the unknown factors of mortgage rates and consumer confidence. Any meaningful recovery is more likely to come in the second half of 2026.

We may be near the bottom of demand and price. Tile import tariffs have been split among the offshore manufacturer, the importer, and the final customer. However, domestic producers also need modest price increases after two years of rising costs and price decreases. For the moment, pricing remains competitive and margins are tight across the value chain.

Imports play a major role

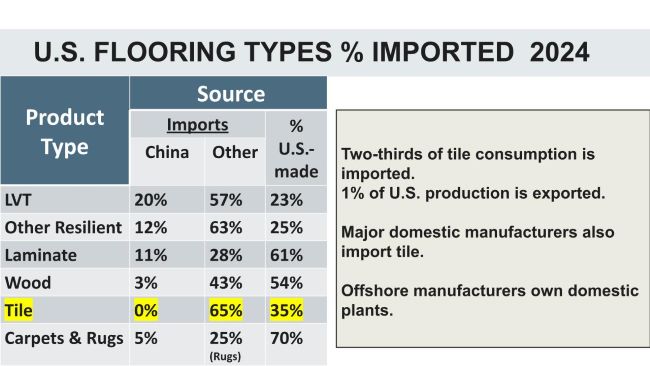

Two-thirds of the tile sold in America is imported. The U.S. does not have enough domestic capacity to meet overall demand. Major U.S.-owned domestic manufacturers still have to import a portion of their products, and some domestic factories owned by non-U.S. companies also import in addition to manufacturing products here.

Italy and Spain continue to lead in import value, while imports from Turkey and India have increased significantly in the past eight years. India’s imports surged starting in 2022, before slowing in late 2024 due to concerns about anti-dumping petitions.

Tariffs distorted the 2025 market. Some companies built inventory ahead of tariffs, some companies shifted a portion of their import sourcing to new suppliers, and some companies shifted some portion of their purchases to domestic supply.

Once tariffs became clearer for European tile imports—at a relatively benign level compared to much worse possible outcomes—uncertainty shifted to other supply countries, such as Mexico, Brazil, and India.

Despite these disruptions, imports will remain essential to the U.S. market, and domestic producers will continue to rely on both their own output and purchases from offshore partners.

Consolidation everywhere you look

Across the flooring and building products industries’ value chain, consolidation continues to reshape the competitive landscape. Mega retailers—Home Depot, Lowe’s, Floor & Decor—have grown from holding a 25% share of the residential remodel retail flooring market in 2016 to more than 40% today. Recent acquisitions in building products by Home Depot and Lowe’s are an aggressive strategy to access more of the total addressable market with a broader product range and through new and multiple channels to more end markets.

Meanwhile, flooring distribution also continues to consolidate, though deal activity slowed in 2025 compared to the flurry of acquisitions between 2021 and 2023. However, merger and acquisition (M&A) activity will pick up as the market recovers. Private equity remains heavily invested in tile distribution, such as Transom Equity’s platform Artivo Surfaces, which combines Virginia Tile, Galleher-Duffy, and Walker Zanger.

Manufacturing M&A has been limited. AHF’s purchase of Crossville stands out. Very recently, AHF acquired Wellmade’s U.S. LVT plant and Beaulieu acquired Congoleum. The overarching trend is fewer players, larger platforms, and a growing divide between highly capitalized companies and smaller independent businesses.

A complicated economy—and tile feels it

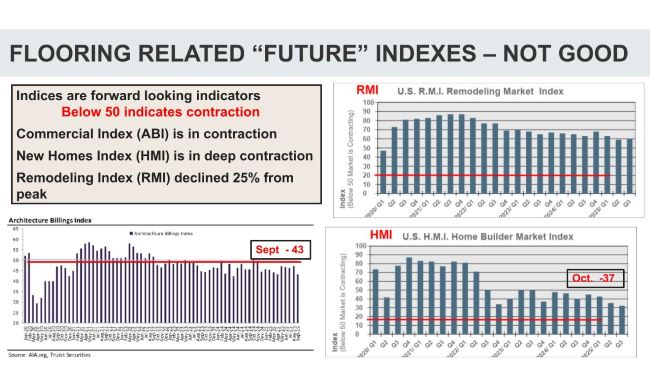

The U.S. economy presents a confusing picture. GDP and the stock market remain positive, but the prospect of even higher inflation, record-low housing affordability, relatively high mortgage and home equity interest rates, and slowing job growth weigh heavily on consumers.

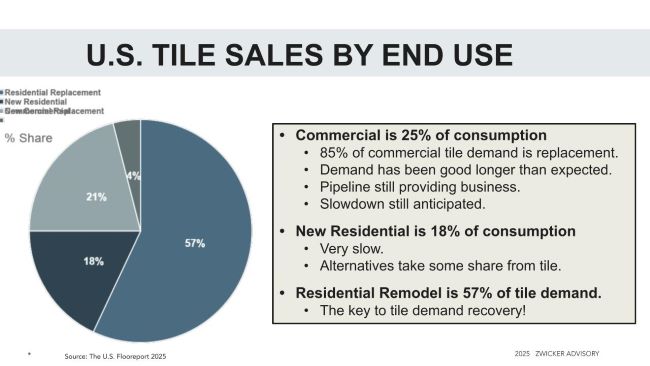

Commercial is a bright spot, representing 25% of tile demand. It has held up better than many expected due to a healthy project pipeline. But pipeline work eventually runs out, and we may be nearing that point. Thankfully, commercial replacement is strong when there are fewer new projects.

However, housing is the weakest link.

- Existing-home sales are stuck at 4 million units, similar to 2009 levels. This stalls remodeling.

- Over half of homeowners have mortgages at 4% or lower, which means they don’t want to move.

- A doubling of the average home price since 2020 and 6% mortgage rates make homes unaffordable.

Residential remodel—about 60% of tile consumption—is the most important driver of tile demand. So, the pivotal issue is consumer sentiment, which averaged 90–100 before COVID. Post-COVID consumer confidence declined to 60–70 and in early November was only 50! This clearly tells the story: consumers remain in a wait-and-see mode.

Hope for a turnaround

Despite the headwinds, several long-term fundamentals support eventual recovery:

- Demographics: Family formation and aging housing stock can drive future demand.

- Massive homeowner equity: A powerful engine for remodeling once interest rates drop.

- Pent-up renovation need: Years of deferred projects have created a backlog.

- Mortgage interest rates: A return to the mid-5% range could reignite home sales.

- Resilient consumers: Historically, American consumers bounce back faster than expected.

Morgan Stanley suggests mortgage rates would need to be 5.5% to drive a 5+% increase in existing-home sales and start a recovery of new-home sales. If that happens, 2026 will be a modest recovery in tile demand followed by stronger growth in 2027.

Guidance for leaders

At the risk of offering advice, I believe these actions are useful during these uncertain times.

- Strengthen product differentiation—large-format, outdoor, and wall tile are growth categories.

- Be agile with multiple supply options—both domestic and imported.

- Use a price-for-profit strategy—marketshare is not always more important than using price as a profit tool.

- Manage cash carefully—delay large expenditures until conditions improve.

- Prepare now for growth or sale of the business—this takes time. Get expert advice.

- Above all, invest in your people—talent is the hardest asset to find and replace.

Looking toward 2026

The tile industry has endured three difficult years, but it is stabilizing. The key variables—mortgage rates, consumer confidence, and tariff clarity—are moving slowly, but hopefully in the right direction. If no major shocks occur, 2026 may finally represent the beginning of the next upcycle.

As I’ve said many times to the tile industry: hang in there. We will get to the other side.

Bruce Zwicker

Bruce Zwicker, Founder and CEO of Zwicker Advisory, has more than 20 years of success growing public, private, and private equity-owned businesses domestically and globally. His experience is across manufacturing, distribution, and retail in the building products sector. He provides customized services in North America and Europe to help CEOs, boards and investors in matters of strategy, governance, executive teams, organization structure, business development, and buying and mergers and acquisitions. He can be reached at 410-903-8357 and[email protected].

{kind=link}